Wealth doesn't trickle down – it just floods offshore

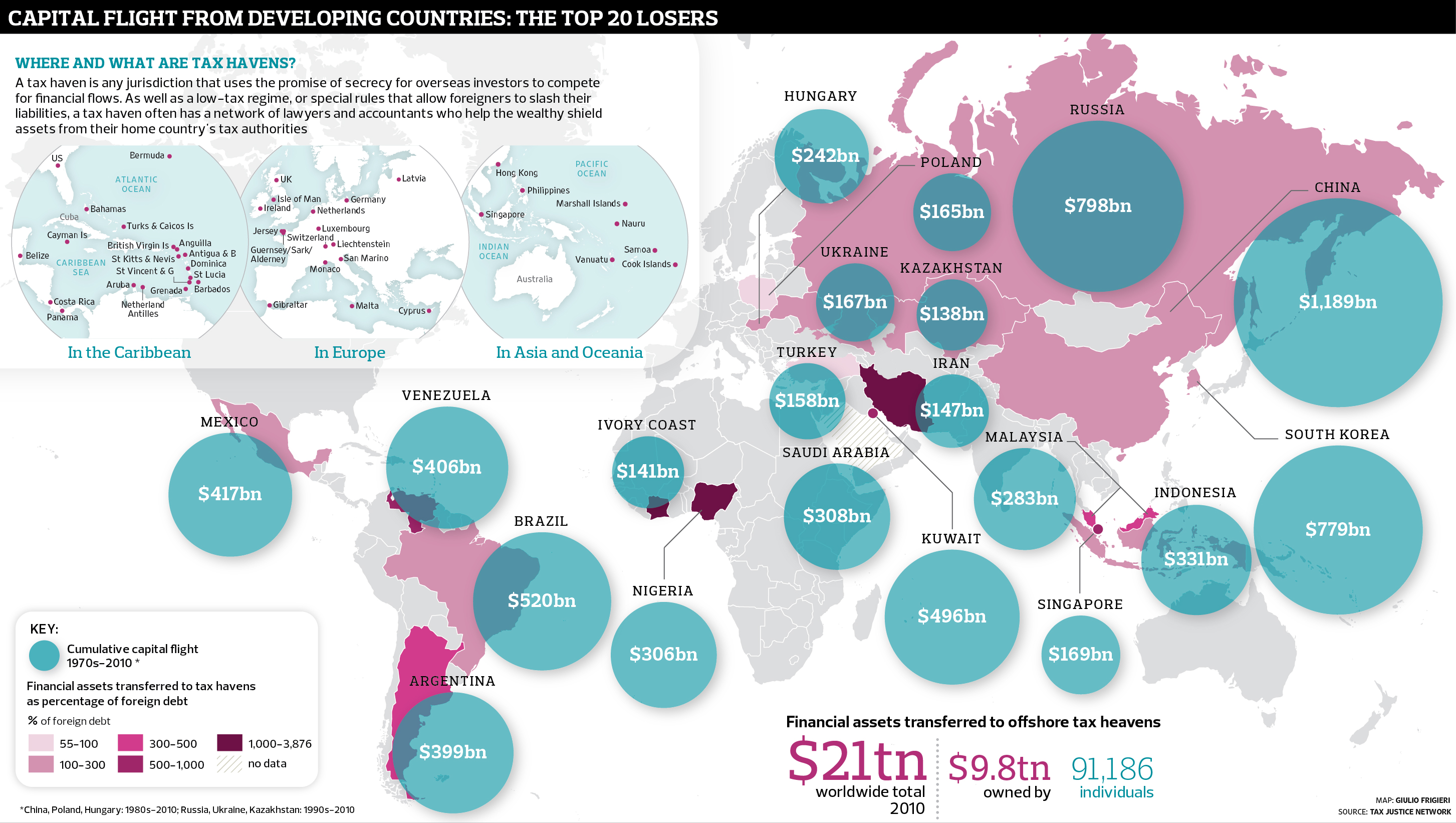

A far-reaching new (British) study suggests a staggering $21 trillion in assets has been lost to global tax havens. If taxed, that could have been enough to put parts of Africa back on its feet – and even solve the euro crisis according to a report in the British paper the Guardian guardian.co.uk.

A far-reaching new (British) study suggests a staggering $21 trillion in assets has been lost to global tax havens. If taxed, that could have been enough to put parts of Africa back on its feet – and even solve the euro crisis according to a report in the British paper the Guardian guardian.co.uk.

(See how the Vincentian Family in Great Britain is playing a role in this issue.)

Capital flight Illustration: Giulio Frigieri for the Observer (click here for a larger version of this graphic)

{kind=link}

The world’s super-rich have taken advantage of lax tax rules to siphon off at least $21 trillion, and possibly as much as $32tn, from their home countries and hide it abroad – a sum larger than the entire American economy.

James Henry, a former chief economist at consultancy McKinsey and an expert on tax havens, has conducted groundbreaking new research for the Tax Justice Network campaign group – sifting through data from the Bank for International Settlements (BIS), the International Monetary Fund (IMF) and private sector analysts to construct an alarming picture that shows capital flooding out of countries across the world and disappearing into the cracks in the financial system.

…

Milorad Kovacevic, chief statistician of the UN Development Programme’s Human Development Report, says both the very wealthy and the very poor tend to be excluded from mainstream calculations of inequality.

“People that are in charge of measuring inequality based on survey data know that the both ends of the distribution are underrepresented – or, even better, misrepresented,” he says.

“There is rarely a household from the top 1% earners that participates in the survey. On the other side, the poor people either don’t have addresses to be selected into the sample, or when selected they misquote their earnings – usually biasing them upwards.”

Inequality is widely seen as having increased sharply in many developed countries over the past decade or more – as described in a recent paper from the IMF, which showed marked increases in the so-called Gini coefficient, which economists use to measure how evenly income is shared across societies.

Globalisation has exposed low-skilled workers to competition from cheap economies such as China, while the surging profitability of the financial services industry – and the spread of the big bonus culture before the credit crunch – led to what economists have called a “racing away” at the top of the income scale.

However, Henry’s research suggests that this acknowledged jump in inequality is a dramatic underestimate. Stewart Lansley, author of the recent book The Cost of Inequality, says: “There is absolutely no doubt at all that the statistics on income and wealth at the top understate the problem.”

The surveys that are used to compile the Gini coefficient “simply don’t touch the super-rich,” he says. “You don’t pick up the multimillionaires and billionaires, and even if you do, you can’t pick it up properly.”

In fact, some experts believe the amount of assets being held offshore is so large that accounting for it fully would radically alter the balance of financial power between countries. The French economist Thomas Piketty, an expert on inequality who helps compile the World Top Incomes Database, says research by his colleagues has shown that “the wealth held in tax havens is probably sufficiently substantial to turn Europe into a very large net creditor with respect to the rest of the world.”

In other words, even a solution to the eurozone’s seemingly endless sovereign debt crisis might be within reach – if only Europe’s governments could get a grip on the wallets of their own wealthiest citizens.

Tags: poverty, Poverty Analysis, strategies, Taxes, VIP